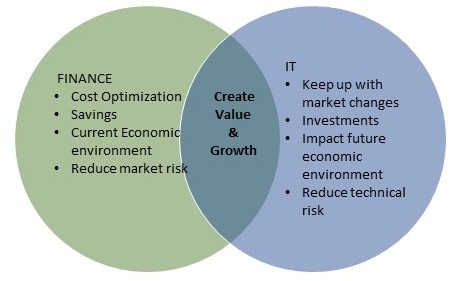

Both Finance

and IT work towards the same goals for the company—create growth and value. But

the way both functions want to achieve the goals differ, which inherently leads

to a conflict. Finance wants to control its SGA expenses and relate it to

revenue trends while IT expenses tend to follow the quickly changing technology

marketplace. But as Gartner managing vice president Barbara Gomolski said very rightly “IT (Cost Optimization) also means that

simply cutting the IT budget and waiting until the economic environment is more

favorable to make digital investments is a flawed approach to remaining

competitive.”[i]

So how should the IT department work with finance to better plan for

its expenses. Let’s examine this in the context of top-down

and bottom-up budgeting processes. A lot has been written about both the

budgeting process and the pros and cons of it. Applying the top-down approach singularly to IT

expenses would lead to a number based on previous year trends. Adjustments will be based on revenue trends

to maintain a specific target of IT expenses as a percentage of revenue. While this process would be faster and

aligned with company goals at a high level it would miss the details and the needs

of the IT department itself. This process would also not take into

consideration the innovation and modernization investments that might be needed

in specific areas. The investments would

be dependent on the current economic environment—if the revenue trend looks

good, IT expenses might be increased and vice versa if revenue trends are not

positive. This in turn might increase

the technical and competitive risk of the company as digital investments are

becoming essential to maintaining competitiveness in any industry.

So how should the IT department work with finance to better plan for

its expenses. Let’s examine this in the context of top-down

and bottom-up budgeting processes. A lot has been written about both the

budgeting process and the pros and cons of it. Applying the top-down approach singularly to IT

expenses would lead to a number based on previous year trends. Adjustments will be based on revenue trends

to maintain a specific target of IT expenses as a percentage of revenue. While this process would be faster and

aligned with company goals at a high level it would miss the details and the needs

of the IT department itself. This process would also not take into

consideration the innovation and modernization investments that might be needed

in specific areas. The investments would

be dependent on the current economic environment—if the revenue trend looks

good, IT expenses might be increased and vice versa if revenue trends are not

positive. This in turn might increase

the technical and competitive risk of the company as digital investments are

becoming essential to maintaining competitiveness in any industry.

In a bottom-up budgeting scenario, the IT function would do

a detailed analysis of needs and put together a budget that aligns very well

with the goals of the IT function. All the participants would need to

coordinate with each other to understand the cost impacts of various projects/changes.

It would also foster the innovation and reduction of technical risks with investments

based on the changes in markets. With this

method, the IT function may be aligned internally regarding the investments but

it might not be fully aligned with the goals of the company since the company

must balance the needs for investments in IT vs. investments needed in other

functions.

To make sure budgets and financial plans are aligned across functions

and there is commitment from leadership, there must be a step of goal alignment

with budgets between the top-down and bottom-up approaches. Goal alignment

meetings should be conducted with a comparison of investments and budgets to the

goals of the company and the function to make sure that prioritization of

expense and investment is done based on the strategic goals of the company

while keeping in the mind the needs of the functions too. This prioritization exercise is imperative to

make sure the functional goals are aligned with the strategic goals of the

company and that the budgeting exercise mirrors this.

As stewards of the company’s finances, financial planning &

analytics (FP&A) analysts should guide the process of alignment of budgets

to goals and prioritization of investments within the company and functions.

FP&A should partner with business to help them make appropriate decisions regarding

the best use of limited resources based on data and analytics.